The banking sector is changing due to millennials and Gen Zers’ growing need for a digital banking experience. Technology appears to be involved in every part of the banking sector, from retail and mobile banking to start-up neobanks. The impact of technology will propel banking toward a digitized future.

Let’s look at the hottest technology trends in the banking sector and the positive changes they trigger.

Banking Technology Trends 2022

The banking sector has been late to the technology party but is making up for lost time with a vengeance. Financial institutions are under pressure to offer digital services that match or exceed those of the Big Tech firms and keep pace with the changing needs of their customers. Here are six technology trends to transform the banking sector over the next few years.

AI and Machine Learning

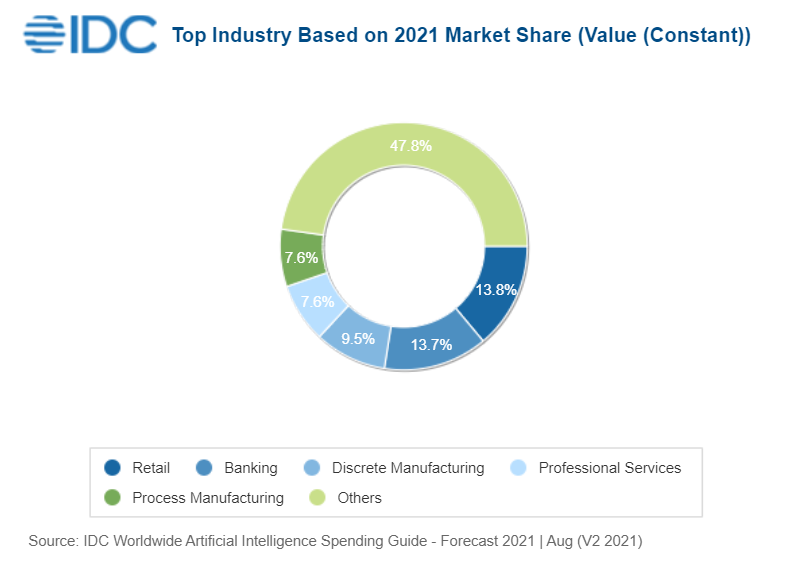

According to the Insider Intelligence survey of banking executives, artificial intelligence (AI) is one of those technologies that will significantly impact banking by 2025. IDC predicts that between 2021 and 2025, the financial services sector will spend roughly 14% of the $204 billion that will be spent yearly on AI, placing it second only to the retail sector in terms of spending.

One of the most significant impacts of AI and machine learning (ML) on the banking industry has been increased efficiency and automation. For example, ML algorithms analyze large amounts of data, identify patterns and trends, and make predictions to improve customer service and fraud detection. In addition, machine learning for banks is also used to develop better financial models and to automate repetitive tasks, such as loan application processing.

Embedded or Contextualized Finance

Customers assume that all their financing alternatives will be integrated, not added as a separate, extra step, into the purchasing process. Banks can implement these features by creating embedded finance solutions. Embedded banking architecture enables collaborations with other businesses to integrate banking and finance services into daily client goals. To meet service expectations and develop real-time middle office processing capabilities like credit arbitration, banks are laying the groundwork for Application Program Interfaces (APIs).

Businesses that adopt embedded finance solutions can provide more individualized solutions, improve risk management, and boost client loyalty. According to Lightyear research, embedded finance will increase from $22.5 billion in 2020 to approximately $230 billion by 2025.

Embedded finance can be the end of banking as we know it. With embedded finance, companies can place financial services exactly where their users need them, at the right moment in the customer journey.

Read: A Complete Guide To Handling Business Resources

Hyper-Personalized Banking

Hyper-Personalized Banking is the next evolution in banking and personal finance. It is the ultimate in bank personalization, where the customer- and product-driven experiences are defined by the individual needs of each and every customer. Hyper-Personalized Banking allows customers to approach their personal financial goals in a more comprehensive, personalized, and integrated way.

This type of banking goes beyond simply offering products and services that meet customers’ needs; it also considers their personal preferences and lifestyles. For example, a hyper-personalized bank might offer special perks and rewards to customers who frequently travel or have young children. Or, a bank may use AI to provide personalized financial planning or investing advice. By taking the time to understand each customer’s unique needs, hyper-personalized banks can provide a level of service that traditional banks simply cannot match.

Neobanks

Neobanks are financial institutions that provide digital-only banking services. This means that they don’t have physical branches and often don’t offer credit products like loans or lines of credit. Instead, they focus on providing modern banking services that are convenient and easy to use. This includes mobile check deposits, person-to-person payments, and budgeting tools. Neobanks have gained popularity because they can offer these services at a lower cost than traditional banks. They also don’t require customers to come into a branch to open an account or perform other everyday tasks. As a result, neobanks are appealing to a new generation of consumers who are used to managing their finances online.

Neobanks offer many of the same services as traditional banks but without the expensive brick-and-mortar locations. This allows them to pass on the savings to their customers through lower fees and higher interest rates. In addition, neobanks are often more convenient than traditional banks, as they can be accessed 24/7 from anywhere with an internet connection.

Read: Top 3 RPA Benefits For A Business

Super Apps

In recent years, we’ve seen the rise of super apps like WeChat and Grab. These all-in-one platforms offer a wide range of services, from messaging and payments to food delivery and ride-hailing. There are already several super apps in operation in Asia, including Paytm in India and Alipay in China. These apps allow users to manage their finances, make payments, and easily transfer money. Apps such as Uber and Airbnb have been incredibly successful in disrupting traditional businesses.

Now, the super app model is set to revolutionize banking.

So what does this mean for traditional banks? They’ll need to start offering a more comprehensive range of services if they want to keep up with the competition. That could include everything from peer-to-peer payments to in-app spending tracking. And we can expect to see more partnerships between banks and other businesses as they look to offer their customers a seamless all-in-one experience.

Banking-as-a-Service (BaaS)

Instead of providing a full range of services, BaaS will primarily focus on providing easy access to your money. It is a relatively new business model that enables third-party developers to access the core infrastructure of a bank. This allows them to build financial products and services that can be integrated into their own platforms. However, it is still in its early stages of development and has yet to be fully embraced by the banking industry.

BaaS providers offer a wide range of services banks can use to improve their operations and better serve their customers. These services will include customer onboarding, fraud prevention, compliance management, and more. Banks that adopt BaaS will be able to reduce their costs, improve their efficiency, and better compete with fintech startups.

These are just some of the trends we expect to see in banking over the next few years. With so much change on the horizon, it’s an exciting time to be involved in the industry.